Taxing Social Security Benefits: Clearing the Confusion

By Laurie Haelen

When the One Big Beautiful Bill Act (OBBBA) was passed in the summer of 2025, there was some confusion in messaging from the Social Security Administration about taxation of benefits.

When the One Big Beautiful Bill Act (OBBBA) was passed in the summer of 2025, there was some confusion in messaging from the Social Security Administration about taxation of benefits.

Many interpreted the OBBBA as a direct reduction in taxes on their Social Security benefits, but this is not the case.

Here is an explanation that hopefully will clarify any questions you have about the new law and the taxing of Social Security benefits.

As I already mentioned, OBBBA does not change the rules for taxing Social Security benefits. The process used to pass OBBBA in the Senate — called budget reconciliation — prohibits any changes to the Social Security program. So, the question is, how does OBBBA help with your taxes in retirement?

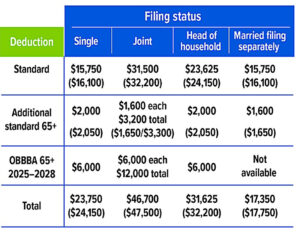

First of all, OBBBA does provide an additional $6,000 deduction for taxpayers 65 and older ($12,000 for a married couple) for tax years 2025–2028. However, this deduction has no direct relationship with Social Security benefits. It is available regardless of whether the taxpayer age 65 and older is receiving benefits. Also, it is not available to taxpayers who are receiving benefits if they are younger than 65.

The deduction phases out at higher income levels: $75,000–$175,000 for single filers, $150,000–$250,000 for joint filers. The taxation of Social Security benefits is based on income. That means the additional senior deduction should reduce the number of people who have to pay taxes on their Social Security benefits by reducing their taxable income. And many of those who do pay taxes will pay less.

According to the White House data, 64% of Social Security beneficiaries did not pay taxes on their benefits before OBBBA and the new senior deduction will increase that to 88%. Yet other analysts indicate that both figures are too high, because they assume that all deductions are applied directly to Social Security income, whereas many seniors receive other taxable income. The nonpartisan Urban-Brookings Tax Policy Center estimates that about half of beneficiaries will still pay some taxes on their Social Security benefits.

The new senior deduction is available regardless of whether a taxpayer takes the standard deduction or itemizes. For those who take the standard deduction, it is in addition to the standard deduction (which applies to all taxpayers) and the already existing additional standard deduction for taxpayers age 65 and older. The combination of all three deductions could result in a substantial reduction in taxable income. Below are the deductions for tax year 2025, with deductions for tax year 2026 in parentheses.

The tax liability for Social Security benefits is based on your combined income, defined by the IRS as your adjusted gross income plus tax-exempt interest plus one-half of your Social Security benefits.

If your combined income exceeds a base amount of $25,000 for single filers or $32,000 for joint filers, you may owe federal income taxes on up to 50% of your Social Security benefits. If your combined income exceeds a higher base amount of $34,000 for single filers or $44,000 for joint filers, you may owe federal income taxes on up to 85% of your benefits.

Considering these rules, the only taxpayers for whom taxation of benefits will be completely eliminated by the new law are those whose combined income drops below the $25,000/$32,000 base amount.

Whether or not your Social Security benefits are taxed, the new senior deduction should reduce your tax burden to some extent. Unfortunately, the implementation likely comes with a long-term effect on the Social Security and Medicare programs, which are funded in part by, you guessed it, taxes on Social Security benefits. One estimate suggests that the new deduction will move the expiration date of the trust funds that help fund Social Security and Medicare up from 2033 to 2032, unless Congress takes action to strengthen the programs. There are many solutions that could occur in the meantime, so no way of predicting the trajectory of Social Security’s fate.

Therefore, it behooves us to try to discern to the best of our abilities the best way to take advantage of the myriad changes in the OBBBA because if we have learned anything, we know that how it is tomorrow will likely be different from what it is today. As always, seeking the help of a professional is always a good idea as we navigate the many retirement challenges of today.

Laurie Haelen, AIF (accredited investment fiduciary), is senior vice president, manager of investment and financial planning solutions, CNB Wealth Management, Canandaigua National Bank & Trust Company. She can be reached at 585-419-0670, ext. 41970 or by email at lhaelen@cnbank.com.

Laurie Haelen, AIF (accredited investment fiduciary), is senior vice president, manager of investment and financial planning solutions, CNB Wealth Management, Canandaigua National Bank & Trust Company. She can be reached at 585-419-0670, ext. 41970 or by email at lhaelen@cnbank.com.